For me, the ideal American government would deliver its important but limited functions efficiently and effectively and would raise the money to pay for these activities with efficient, minimally distorting (neutral), and fair taxes following a principle of maximum subsidiarity (decisions made and services performed at the most local levels possible). The government should do fewer things than it does now but should do them better and should fully pay for them with taxes and fees (cyclically balanced budgets).

My unrestrained, radical platform will be presented here at a high level of general principles. Details need to be refined by a political process involving public discussion and are likely to evolve somewhat over time. Links to earlier articles provide additional details. In the very broadest terms Americans should be self reliant and free to work and play as hard as they choose with the government supporting their choices by providing security, the legal foundation and framework of private property and contracts, and an efficient safety net when individual undertakings are not feasible or fail.

The limited functions of the Federal government are enumerated in Article 1 section 8 of the U.S. Constitution. Broadly these are to:

- Develop and maintain our relations with other countries and international bodies and to maintain an Army, Navy and Air Force for the purposes of defending and promoting the security of the United States;

- Establish and enforce the rights to property and contracts and to adjudicate related disputes;

- Provide for public safety;

- Provide an efficient and effective social safety net (welfare);

- “Regulate commerce with foreign Nations, and among the several States;”

- “Coin money, regulate the value thereof, and of foreign coin, and fix the Standard of Weights and Measures;”

- Arrange for the provision of roads and essential infrastructure; and

- Tax, borrow, and levy fees and tariffs to pay for these activities.

Our Social Contract

Sovereignty resides with each individual, who have collectively ceded limited powers to government for the general welfare. Each of us is free, within legal limits on doing harm to others, to lead our own lives and build or work at whatever we choose. Thus the government’s laws apply equally to each of us without regard to our race, religion, sex, or sexual orientation. From this environment of freedom and innovation, America has built the most successful economy in the world.

When building companies or developing products, many will fail and try again. The government provides the legal framework (bankruptcy) for resolving such failures. The implicit agreement between citizens and their government is that government will provide a floor—a safety net—whenever a person’s efforts fail or when, e.g., for health reasons, a person is unable to provide for him or herself. The level of the safety net should reflect the level of the country’s income and social consensus and should be designed to achieve its objective as efficiently as possible with careful consideration of the incentives it creates.

Income redistribution: taxation and a guaranteed minimum income

All income (personal and corporate) taxes should be replaced with a comprehensive, flat, consumption tax (Value Added Tax—VAT) and limited progressivity introduced by paying every legal man, woman and child resident a guaranteed minimum income. US federal tax policy, Cayman Financial Review July 2009 Each recipient of these monthly guaranteed income payments would be required to set aside a minimum amount for health insurance (chosen by each person or family in the competitive market place) and a minimum amount for retirement (invested in qualifying retirement funds in the competitive market place). Saving social security

As the guaranteed minimum income should be at a level sufficient to minimally support life’s basic needs, supplements such as unemployment or disability insurance would not be needed or provided. However, disabilities acquired from military or public safety service should receive additional income support.

Health care

Each person will be responsible for paying for at least part of routine medical care (the copay required by the insurance they have chosen) and will thus care about its cost. The cheapest insurance policies will be limited to major medical expenses (catastrophic health insurance). As everyone will be required to contribute monthly to a health savings account from their guaranteed minimum income, most people will chose to use such funds to buy health insurance, which would not be tied to employment or an employer.

Doctors and hospitals will be required to make medical service costs transparent. On that basis, patients, in consultation with their doctors, will decide the level of care and treatments to receive. These measures will introduce normal market competition into the provision of medical care that is currently absent, which will improve its quality and lower its cost.

Education

Equal access to quality education is a critical element in maximizing opportunity for all and the wealth of our society and each person in it. The public school system has often failed in this objective. While the wealthy can afford to put their children in private schools when the neighborhood school is of poor quality, lower income families generally cannot. Every K-12 aged child will receive a tuition voucher that covers the cost of state provided education. The amount will generally vary from state to state (or school district to school district). The voucher can be used to attend the local neighborhood public school with no additional cost, or any private school the family chooses, which might incur additional costs. Schools eligible to receive such vouchers must meet minimum education standards set by the state and must disclose the performance of their students on state administered achievement tests. This information must be available to the public. The learning progress of each child is more important than the average level of achievement of each school’s students as some schools might well specialize in slow or problem learners and performance data should reflect this distinction. The neighborhood school has the advantage of being easier to get to every day and will normally be chosen by families if it provides a good education. The argument for universal tuition vouchers goes beyond providing a level playing field to all. It also introduces the competition for students that is the basis for good quality, low cost goods and services in every other area of our economy.

Access to higher education raises different issues. Those with the aptitude and desire for a college or postgraduate degree can significantly increase their lifetime incomes as a result. It would hardly be fair to tax the general public to subsidize the higher education of those who will become wealthier as a result. However, the tuition loans that may be needed by those from lower income families to make this investment would be hard to get without insurance against default. Many states also provide community (or Jr.) colleges at public expense that provide training in various trade skills as well as four year college preparatory courses. These seem to have often been successful in leveling the playing field. The optimal structuring of higher education subsidies (e.g. between insurance guarantees and tuition subsidies) needs further examination.

Monetary and Financial Policies

Government policies that affect business should be as rule based and transparent as possible. Monetary policy stands out as a particularly important area in which clearer rules are needed. A currency with stable real value (purchasing power) is an important part of the foundation of efficient free markets. At the very minimum the Federal Reserve’s mandate should be tightened as provided in the very pragmatic Federal Reserve Accountability and Transparency Act of 2014. This act would require the Fed to chose an operational rule, from which it could depart only with an explanation to Congress of its reasons. A deeper review of options is proposed by the Centennial Monetary Commission Act of 2015. I have proposed a more radical reform in the spirit of the gold standard but with tighter rules and an anchor of a large number of goods rather than just gold. The supply of this currency, which ideally would become the global currency, would be regulated by the market using currency board rules and “indirect redeemability.” A hard anchor for the dollar.

The banking and financial sector are currently smothered with detailed regulations the compliance cost of which are driving smaller banks out of business. Under the Dodd Frank law adopted after the financial crisis of 2008, the largest five American banks have grown even larger (in absolute terms and as a share of the banking sector) than they were in 2008. Regulators, despite (or because of) their detailed banking regulations have failed to make banks safer and have slowed the competitive process of producing better and cheaper services. Bank owners and market preferences should regulate risk taking by banks.

Bank regulation by the government should focus on broad principles with strong owner accountability. Bank capital requirements should be raised and the no bail out rules strengthened. Bank owners and investors should absorb any bank losses. The payment services of banks should be isolated from the rest of its lending and investing business by adopting the Chicago Plan of one hundred percent reserve requirements against current account deposits, and virtually all other regulations (other than accounting and reporting standards) should be dropped. Larger banks will develop their own risk weighted capital requirements for their internal use, but the government’s capital requirements should state the minimum required leverage ratio (ratio of core capital to total assets) and set it at a high level. Changing direction on bank regulation, Cayman Financial Review April 2015. A bill now in congress moves in this direction: The Financial Choice Act

Business activities and regulation

The government should only provide services that that private sector can’t. It should provide the legal and regulatory framework for the private economy rather than compete with it. Though the approaches to providing “public goods” such as police, courts, prisons, firemen, parks, highways, airports, etc. have varied over time, they are almost always paid for by the government (i.e. collectively by tax payers) and should be provided efficiently at the level expected by the public. Publicly funded and privately produced goods and services are often sources of hard or soft corruption. Rather than over charging for services or paying bribes to win contracts (hard corruption), soft corruption exploits influence on government to obtain contract terms or regulations favorable to particular firms (“rent seeking”). The government’s purchases of goods and services from the private sector should be governed by transparent rules that promote competition among suppliers. This is easier said than done. Open the Books

While the government is involved in and trying to do far too many things, it doesn’t do many of them very well. Of those services the government needs to provide, states generally perform better than the federal government though performance varies across states. In Maryland, where I live, I was able to register my Limited Liability Company on line in about 30 minutes start to finish. Registering my car and updating my driver’s license is quick and easy. However, it took me months to obtain a statement of my residency from the U.S. Treasury and a personal trip to the State Department to have it certified to provide to the National Bank of Kazakhstan before they could pay me for my services. Getting a passport or green card is more complicated and takes longer than they should. The government should do much less and do it much better.

Those in the government who believe they can judge better than competitive private markets how best to allocate resources (what to invest in and produce) are generally wrong. Moreover, they establish an opportunity and thus incentive for corruption.

The government’s regulation of private businesses in the interest of public safety, environmental protection, and market competition should be limited and subject to very serious cost/benefit tests. Cost/benefit analysis unavoidably reflects subjective judgments but their role should be limited to the extent possible by full transparency of the basis of any assessment. Competitive capitalism vs. the other kinds.

Foreign policy and national security

The purpose of our foreign policy is to serve American security interests and the international rule of law under which American’s can explore the world and American businesses can compete globally on a level playing field. Our security requires a strong military, but it also requires the skillful use of diplomacy. Our military must be structured for defense, not offensive wars of our choosing. Our 2003 war in Iraq and subsequent developments in the Middle East have cost many lives (some American) and treasure, undermined our moral authority, and seriously damaged our security. Our foreign policy should be one of “restraint.”

Our relations with other countries should be based on shared interests consistent with our respect for individual dignity and the rule of law. We should support and, where appropriate, lead international bodies dedicated to developing, promoting, and overseeing compliance with the rule of law internationally. Our international leadership should rest, in addition to our economic and military strength, on our commitment to broadly shared values and standards of behavior. Just as we give up limited amounts of our individual sovereignty to our own government when it serves our individual and collective interests, so should we give up limited amounts of our national sovereignty to international bodies when it serves our national and international interests.

Our economic strength depends in part on providing for a sufficiently strong military in the most economical way possible. Money spent on tanks can be spent on building other businesses and producing goods that we enjoy. The very nature of the relationship between our military and the industries that supply it, what President Eisenhower called “the military industrial complex,” makes achieving this objective very difficult. As argued above, clear rules and transparency are important tools. Our unsupportable empire

Trade

Next to the right to personal property, nothing is as central to our liberty and well being as the right to trade. It is the basis of virtually all of our enormous increase in productivity and thus our standard of living. The government impedes our right to trade with a wide range of often unnecessary or excessive regulations. Restricting our freedom to trade across national borders is also a mistake that reduces our standard of living from its potential.

Trade has destroyed some jobs while creating others. “Since 1900, the portion of the U.S. workforce in agriculture has declined from 41 percent to less than 2 percent. Output per remaining farmer and per acre has soared since millions of agricultural workers made the modernization trek from farms to more productive employment in city factories…. Manufacturing’s postwar share of the labor force peaked at about 30 percent” in 1953 and has since declined to less than 9 percent while manufacturing output continued to climb. “Of the 5.6 million manufacturing jobs lost between 2000 and 2010, trade accounted for 13 percent of job losses and productivity improvements accounted for more than 85 percent.” George Will, Washington Post.

As with domestic, competitive trade, those out-performed in competitive markets suffer, at least temporarily. The safety net for “losers” in the competitive process discussed above is an important feature in our willingness to unleash the benefits of free trade. We must insure that they are adequate. We should support the World Trade Organization (WTO) as well as regional and bilateral agreements that reduce the barriers to trade and promote freer trade. Save trade. Globalization and nationalism-good and/or bad?. Trade and globalization

Conclusion

Our government should assume that each of us is capable of and has the right to make our own decisions and lead our own lives as we see fit. Its role is to protect those rights, in part by protecting us from others, foreign and domestic, who would violate them. We are, however, part of and best flourish within broader communities. Our government should develop legal frameworks to facilitate our interactions and relationships within and across societies both business and personal. Our successful flourishing will also depend greatly on a shared culture of mutual respect and comity.

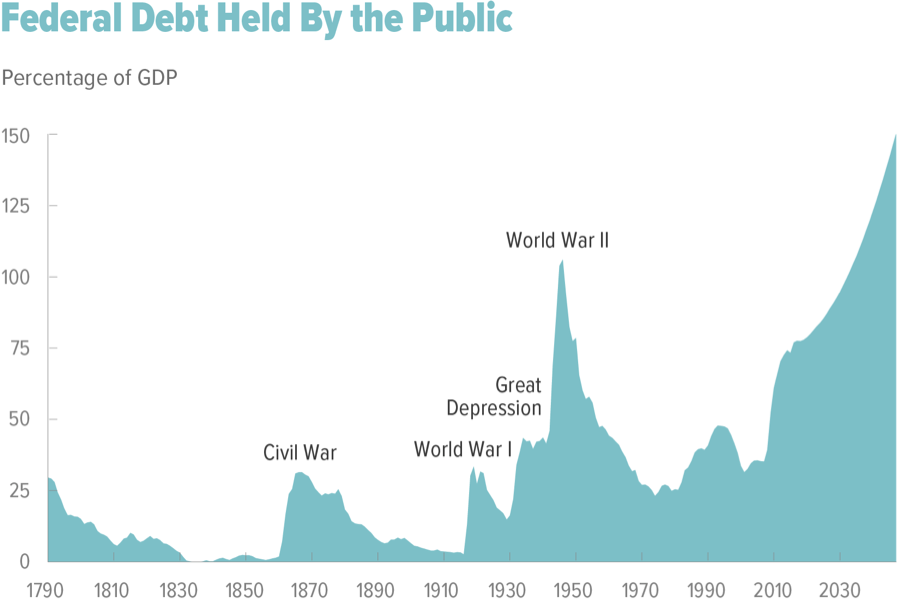

Congressional Budget Office forecasts

Congressional Budget Office forecasts