The elimination of State and Local Tax (SALT) deductions from the proposed tax reforms working their way through Congress has become a hot topic. Fine, but please keep the discussion honest. Sadly my local newspaper, The Washington Post, is not setting a good example: “In-towns-and-cities-nationwide-fears-of-trickle-down-effects-of-federal-tax-legislation”

First a word about tax reform vs tax reduction. We are now in the 9th year of economic recovery, one of the longest on record. It won’t go on forever. Ideally the Federal government’s budget should balance its expenditures and revenue over the business cycle. That allows for aggregate demand stimulating deficits during business downturns. These deficits result from so called automatic stabilizers—the fall in tax revenue from the fall in taxable income plus increased transfer payments to the unemployed. But a cyclically balanced budget also requires budget surpluses during the business expansion phase. The U.S. economy is now fully employed (in fact, unfilled vacancies exceed those looking for work). The Federal Reserve has finally increased inflation to its target rate of 2%. We should now have budget surpluses to make room for the deficits that will follow during the upcoming downturn.

But our fiscal situation is much worse than that. The large increase in “entitlement” expenditures for my greedy generation as we retire (greatly increasing unfunded social security and health benefits) will push our fiscal debt held by the public, now at 77% of our Gross Domestic Product (GDP), to over 150% of GDP within 30 years if current laws remain unchanged. See the figure below.

Taxes will either need to be increased (not reduced) or entitlement expenditures reduced (which means increased less than current law provides). My point is that reducing tax revenue at this time is irresponsible without at least matching expenditure cuts. The proposed tax reforms now in congress would increase the debt by $1,500 billion dollars over the next ten years on a static forecast basis, meaning without taking into account the increased growth and thus tax revenue that might result from the tax reforms, which no one expects to wipe out all of the static forecast of $1,500 billion.

Congressional Budget Office forecasts

Congressional Budget Office forecasts

While it is irresponsible to cut tax revenue at this time, it is highly desirable to reform how that revenue is raised. The existing taxes distort the economy and thus reduce our incomes in a number of ways. They grant favors to many special interest groups via allowing them to deduct specific expenditures from their taxable incomes (i.e. from the tax base). These so called tax subsidies encourage activities over what the private economy would otherwise under take. One very damaging example is the deduction of interest payments by businesses and individuals, which has encouraged excessive borrowing and indebtedness. The most popular of these is the mortgage interest deduction by homeowners. This tax subsidy benefits homeowners relative to renters, i.e. it benefits the wealthier at the expense of the poor. How well meaning middle and upper income American’s can justify this with a straight face is beyond me.

But what about the SALT deductions? By eliminating such deductions, i.e. by broadening the tax base, the same revenue can be raised with a lower tax rate. Other things equal (such as revenue), lower tax rates are good because they influence taxpayer decisions less. For example, companies are more likely to invest in the U.S. rather than abroad if the corporate tax rate is reduced from its current 35%, virtually the highest in the world, to 20%, which is closer to the rate in most developed countries.

Reducing tax subsidies to state and local governments is also good because it reduces an artificial encouragement for larger state and local government expenditures. If Californians are willing to pay more state taxes for larger state expenditures they are welcome to do so. But there can be no justification for transferring federal tax revenue from states with lower expenditures and matching taxes to California and other high spending states. To a large extent the existing SALT deductions transfer income from poorer states to wealthier ones. Who can support that with a straight face?

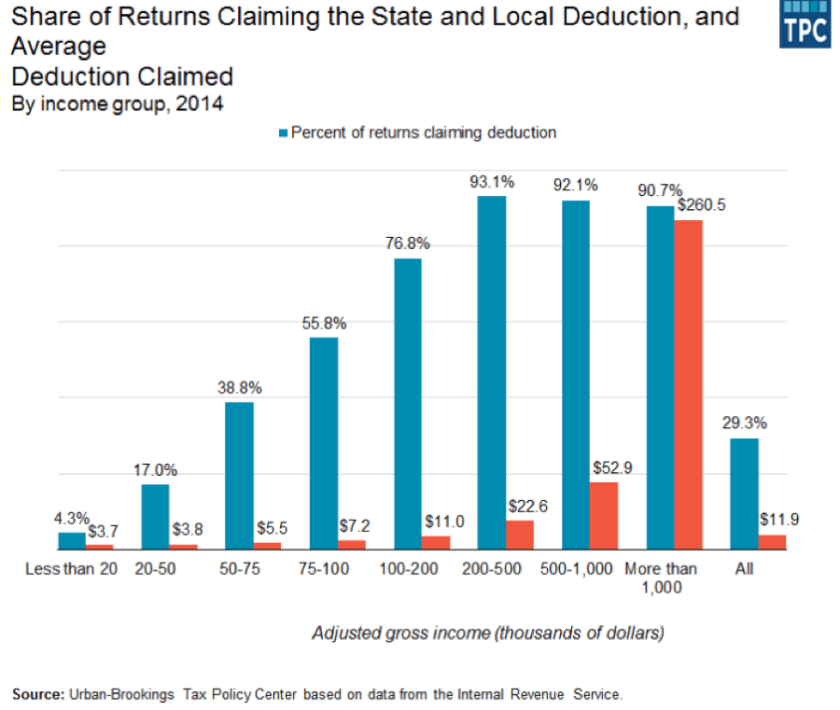

How information is presented can have a significant effect on how it is understood or viewed. How did Renae Merle and Peter Jamison of The Washington Post (see link above) report the proposed elimination of the SALT deduction? They reported that, “In San Diego County, the elimination of what is commonly called the “SALT” deduction could affect about a third of households, said Greg Cox, a member of the board of supervisors. The average middle-income resident would lose a $16,000 deduction.” They failed to note that the third of households affected are the wealthiest third. According to CNBC: “More than half of taxpayers who are earning $75,000 and above claim SALT deductions on their federal income tax returns as do more than 90 percent of taxpayers who make $200,000 or more.”

Furthermore, the figure $16,000 is misleading in two respects. The loss of a $16,000 deduction would increase taxes for a single person earning $200,000 annually by $5,280 at the current tax rate of 33%. However, broadening the tax base by eliminating the SALT and other deductions allows raising the same revenue with a lower tax rate. To measure the actual tax impact both effects must be combined. Current congressional proposals are to reduce the rate for the above person to 25%, which would result in an increased tax of $4,000. None of this would affect the poor directly. I assume that Renae Merle and Peter Jamison were just careless rather than letting their biases get the best of them, but you can make your own judgment.

The SALT deduction cannot be justified on either economic or fairness grounds, but there is sadly a good chance congress will cave in to the pressure from the wealthier states to keep it or at least some of it.