I just finished listening to the Audible version of Thinking the Twentieth Century, a discussion between Tony Judt and Timothy Snyder, recorded just before Judt died in 2010. Judt was a British-American historian, essayist and university professor who specialized in European history. Snyder is an American author and historian specializing in the history of Central and Eastern Europe and the Holocaust.

I found Judt to be a very insightful in his area of political and social history expertise but generally off base on economic issues, which is not his field. I fear that his misunderstanding of trade is widely shared so I will set out some important basics as a contribution to better public understanding. “Science” doesn’t dictate policy, but a correct understanding of the economics of trade is essential if one’s value preferences are to lead to policies that produce your desired result.

Judt describes the increase in American wages for manufacturing workers along with their health and pension benefits over the past several decades leading manufacturing firms to outsource their production to the cheaper labor in (for example) China and thus hollowing out American manufacturing. Almost everything about this description is wrong.

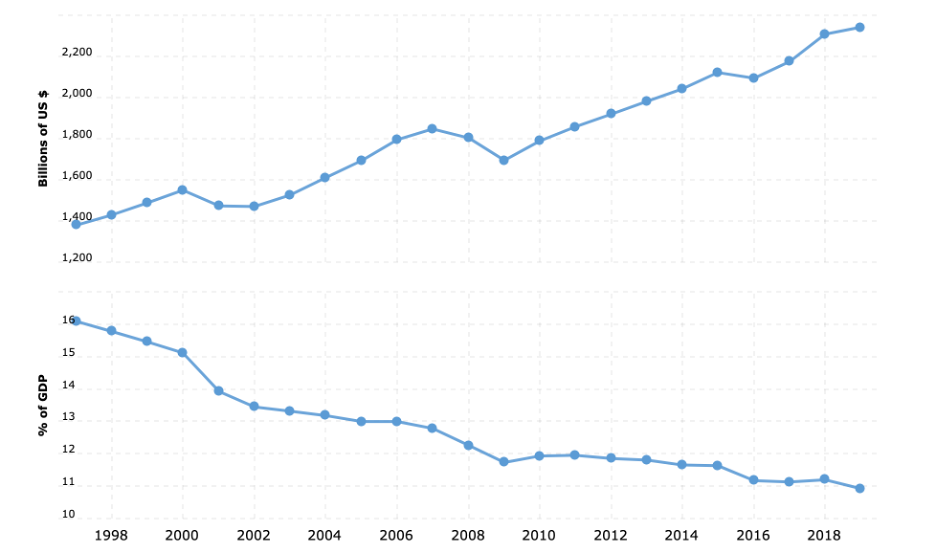

For starters manufacturing output in the U.S. is at an all-time high (prior to Covid shutdowns). Off shorting some of it has not hollowed out U.S. manufacturing. Because manufacturing output has grown more slowly than the economy overall (the upper line below), its share of GDP has fallen (the lower line). Moreover, because of increased labor productivity in manufacturing, fewer workers are needed to produce this increased output (second chart) thus freeing labor to work in other areas and increasing our overall standard of living.

U.S. manufacturing output

Billions of US $ and Percent of GDP

Data Source: World Bank

MLA Citation: <a href=’https://www.macrotrends.net/countries/USA/united-states/manufacturing-output’>U.S. Manufacturing Output 1997-2021</a>. http://www.macrotrends.net. Retrieved 2021-08-16.

But let’s take a closer look at Judt’s statement. If the U.S. shifts some manufacturing offshore, it must pay for it. Instead of paying American workers it must pay Chinese workers, and firms and shipping companies. Fundamentally, a country’s imports must be paid for by its exports (or by capital inflows from the exporting country). Let’s look carefully at each possibility. To simplify, let’s initially assume that there are no capital flows (cross border investments from one country in another) so that trade in goods and services must balance (i.e., pay for each other).

For starters whether labor is cheaper in China than in the U.S. cannot be determined without considering the exchange rate of the dollar for the Chinese Yuan. If exchange rates (not mentioned by Judt) are flexible (determined freely in the market) the fact of an increase in U.S. imports from China (i.e., the offshoring of U.S. manufacturing to China) will depreciate the dollar/Yuan exchange rate. As U.S. manufacturers sell dollars to buy Yuan with which to pay for the goods they now want to buy from China, Yuan will become more expensive (a depreciation of the exchange value of the dollar). The dollar’s depreciation will have two effects. It increases the cost of Chinese labor to U.S. companies and thus will reduce the cost advantage of Chinese labor and reduce the demand for it by U.S. firms. And it will lower the cost of U.S. exports thus making them more attractive in China. While the adjustments will take time, the dollar depreciation will continue until American exports increase and its imports from China moderate until trade balances–our increased exports pay for our increased imports.

If the exchange rates are fixed, as they were in gold standard days, the adjustment in the real effective exchange rate needed to balance trade takes a different form. The initial increase in the demand for Chinese products (outsourcing to Chinese workers) are paid for with dollars. But to preserve the fixed exchange rate, the PBRC (Chinese central bank) must buy these dollars with newly created Chinese currency. This increase in the Chinese money supply will lift prices in China making Chinese exports more expensive in the U.S. and U.S. goods cheaper in China. In short, the real exchange rate adjustment needed to balance imports and exports in this case results from a higher inflation rate in China than in the U.S. while in the first case of flexible exchange rates it results from adjustments in the nominal exchanges rates themselves.

A third possibility is for China to take the extra dollars being spent in China and invest them in the U.S. (or elsewhere) This is the capital flow case in which trade itself does not balance. This was the policy followed by China in the 2000s through 2014. The PBRC would buy the dollars being spent for outsourced Chinese labor (U.S. manufacturers payments to Chinese workers rather than to American ones for the goods they needed) and would invest them in the U.S. If the increase in the Chinese money supply resulting from those dollar purchases was more than was consistent with stable prices in China, the excess money would be sterilized–so called sterilized foreign exchange intervention (the PBRC would create Yuan to buy dollars and would repurchase some of those Yuan back with domestic Chinese securities owned by the PBRC).

To some extent this foreign exchange market intervention by the PBRC was the result of its desire to build up its FX reserves (a kind of insurance policy for exchange rate shocks). However, much of it was to prevent an appreciation of the Yuan that would reduce its exports (it was following an export led development strategy). This policy was much criticized abroad as currency manipulation and ended in 2013-4. Thus, China has financed a significant part of the U.S. governments fiscal debt. https://nationalinterest.org/feature/who-pays-uncle-sams-deficits-26417

Thus, when someone says that something is cheaper to make in China, remember that it must also be that from China’s perspective, something must be cheaper to make in the U.S. in order to pay for what China sends to us. Both sides benefit and the world grows richer.

Spell checking doesn’t understand meaning and grammer.

E.g., “For starters manufacturing output in the U.S. is at an all-time high (prior to Covid shutdowns). Off shorting some of it …”

Do capital inflows to the US represent something “from” the US except the nationality of ownership?

E.g. “Fundamentally, a country’s imports must be paid for by its exports (or by capital inflows from the exporting country)”

Very good short essay on the fundamentals.

Trade flows are outweighed by capital inflows in today’s world so the depreciation of the dollar you mention in the first paragraph doesn’t quite happen. In practice the Chinese sell us their manufactures and we sell them tech stocks and property. Is that a good trade off?

Germany and Japan preserved more of their manufacturing share of output and employment than the US did. By your logic we should not consider that a particularly notable policy success. That doesn’t sound right.

Chinese investment in the US has fall. Before covid trade almost balanced. Is it good or bad if we export to pay for Chinese financing of are fiscal debt? That depends on how the benefits of our government’s use of that money compares to the alternatives.

“Before trade covid almost balanced”. The bilateral goods trade gap was not closing. What are you referring to? https://www.census.gov/foreign-trade/balance/c5700.html

Did China’s FX manipulation strategy end in 2014? Some people think they are using commercial banks which they control to not declare their FX holdings. And clearly the Belgian account was being used for a while to hide their FX purchases….

“Both sides benefit and the world grows richer.” Really?

When a Chinese businessman buys a company in the US, the money to purchase the company flows in to the US accounting system as an “export” but on the Capital Account, it is counted as a negative (to offset the positive of the goods the Chinese businessman might have earned by selling something prior in the USA).

Basically the problem with the description is that terms have inverted connotations, as if “exports” were good and “imports” are bad. A trade “deficit” is a boon to the economy, as it most commonly indicates faster growth (thus imports are demanded). Only in a Great Depression world would it be a deficit from “selling the furniture out of the house to buy food.” (Exports ‘good’ = sell the furniture)